Sign up for the QMED & MD+DI Daily newsletter.

State of the Latin American Dental Bone Graft Substitute Market

Qmed Staff

March 20, 2017

6 Min Read

.svg?width=850&auto=webp&quality=95&format=jpg&disable=upscale "State of the Latin American Dental Bone Graft Substitute Market")

The market for dental bone graft substitutes in Latin America is being shaped by technological innovation and attempts to reduce disease transmission.

Salma Mashkoor and Jeffrey Wong

The Latin American market for dental bone graft substitutes includes the bone graft substitute and dental membrane markets in Brazil, Argentina, and Mexico. These markets are growing in response to technological innovation, as well as ongoing attempts to reduce disease transmission. However, a lack of government insurance coverage restricts the growth potential in all three regions.

Brazil represented the largest market in 2016, both in terms of value and growth. Brazil is the second-largest market for dental implants across the globe, trailing the United States. The relatively active Brazilian implant market is explained in part by the country's large population, exceeding 200 million in 2016. Furthermore, there are is a large number of dentists in Brazil, outnumbering the population of dentists in the United States.

The highest priced market is Mexico, where a rising incidence of dental tourism is stimulating growth. Despite the fragile state of the economy, Mexico has continued to lure in international customers--primarily Americans--with its affordable dental products. In addition to encouraging growth in procedural volumes, the foreign customer base is also less reluctant to opt for pricier procedures as they continue to be relatively inexpensive in Mexico.

Disease Prevention

In recent years, there has been a rising concern regarding the safety and quality of bone graft substitutes, prompting regulatory agencies to become stricter in their policies. Tissue banks have consequently claimed most of the control over allograft distribution in hopes of establishing better sanitation. In fact, in some regions such as Argentina, allograft materials from major companies have been pulled from the market, resulting in a complete reliance on tissue bank allografts. To ensure tissue quality, regulatory agencies have tightened their guidelines, warding off potential consumers. These guidelines tend to be intimidating, as doctors are required to report and process copious amounts of information. Allograft materials are generally inexpensive, especially when compared with xenografts. As the inexpensive sector of the market becomes less popular, the overall bone graft substitute market will experience an upsurge in value.

Technological Innovation

Nonresorbable barriers are made of thin sheets of materials, mainly polymers. They are stable, non-degradable, and biocompatible. However, a second surgical procedure is required for removal, which represents a limitation and involves a potential risk to the newly regenerated tissues. Finally, membrane exposure is frequent, increasing the risk of secondary infection. Bioresorbable membranes, or simply resorbable membranes, offer many advantages over nonresorbable materials. Apart from the fact that there is no need for a second surgical intervention for removal of the membrane, they present improved soft tissue healing and reduce the chance of bacterial contamination. Most researchers and clinicians agree that in comparison to nonresorbable membranes, sites treated with resorbable membranes present a lower rate of complications.

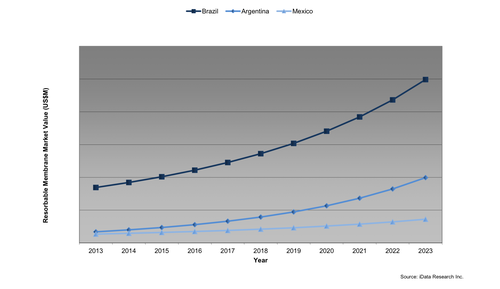

Growth of the dental membrane market in Latin America is primarily being driven by a continuous shift toward resorbable products. Across the board, dental professionals are making attempts to reduce the risk of contamination and spread of disease in bone grafting procedures. In hopes of performing safer dental treatments, this has facilitated the movement toward resorbable products, which are priced at a premium in comparison to titanium-based nonresorbable products. On average, resorbable membranes are more expensive than nonresorbable membranes of equivalent size. As resorbable membranes continue to comprise a larger proportion of membranes sold, they will help augment market growth.

Lack of Government Dental Insurance Coverage

The overall market for bone graft substitutes and dental membranes in Latin America is limited by a lack of governmental dental insurance coverage. In all of the regions considered, there is no insurance coverage for dental implant or bone graft procedures. As such, the bulk of the population does not have the funds to support such treatments. As a result, numerous local companies have emerged in each country, offering similar products at a marked-down price. These smaller competitors have appealed to the public through their attractive product offerings and affordable prices, thus prompting total market growth to slow down. Even multinational corporations have engaged in price cuts to compete with the vast assortment of inexpensive, local alternatives, furthering restricting the growth potential of the market.

Competitive Analysis

Due to developing interests in minimizing disease and cutting costs, there has recently been a shift in the companies involved with the dental bone graft substitute and membrane markets. First, a number of local competitors have emerged, offering products at marked-down price points. As there is no government insurance for bone graft substitute procedures and the economy is relatively fragile, these cheaper products are able to accommodate to the needs of the wider public. In Brazil,a number of tariffs and expenses have been introduced to prevent international competitors from penetrating the market, thereby providing local companies with a large competitive advantage.

Tightening regulations have revealed multiple competitors that did not meet the renewed regulatory standards, thereby forcing them to close shop. This trend had been especially impactful in Mexico, as it led to the loss of market leaders such as Geistlich and Zimmer Biomet.

Nonetheless, Geistlich managed to maintain a significant presence in Brazil and Argentina. Many dentists are well acquainted with their products, having had early exposure to them in dental schools. The company benefited from selling the most recognized brand of dental bone graft material, Bio-Oss, which allowed it to hold significant market share in the xenograft segment. It also sells Bio-Gide dental membranes. The company has a long history of proven clinical data documenting the efficacy of Bio-Ossand Bio-Gide. A strong foundation in scientific research and extensive product base will ensure Geistlich maintains its presence on the market for the foreseeable future.

References

Mexico Market Report Suite for Dental Bone Graft Substitutes and Other Biomaterials 2017 - MedSuite

Brazil Market Report Suite for Dental Bone Graft Substitutes and Other Biomaterials 2017 - MedSuite

Salma Mashkoor is a research analyst at iData Research and was the lead researcher for the 2017 Latin America Dental Bone Graft Substitute Report Suite, which includes reports on Brazil, Argentina, and Mexico. Her current work includes the 2017 Latin America Dental Implant, 2017 Latin America Bone Graft Substitute, and 2017 U.S. Dental Materials Report.

Jeffrey Wong, is the strategic analyst manager at iData Research and has been heavily involved with the company's dental division throughout his tenure. As a research analyst, he led several research projects on the global dental markets including dental prosthetics, digital dentistry, CAD/CAM materials, dental implants, bone graft substitutes, hygiene, dental imaging, and dental lasers.

[Images courtesy of KJERSTIN MICHAELA/PIXABAY.COM and IDATA RESEARCH]

About the Author(s)

You May Also Like

.png?width=300&auto=webp&quality=80&disable=upscale)