Sign up for the QMED & MD+DI Daily newsletter.

Future Risks and Dangers

6 Min Read

.svg?width=850&auto=webp&quality=95&format=jpg&disable=upscale "Future Risks: How Biomedical Companies Navigated Turbulent Economic Times")

After five relatively good years, the medical device industry faces a more challenging future, with significant risks to growth and profitability. Regulation of medical devices is growing, with new certifications and testing required in the United States by FDA, many under the terms of the 510(k) process. This issue has already raised costs and extended time to market and realization of revenue for several firms. As implants increasingly include elements of pharmaceuticals in them (e.g. drug coated stents, joint replacements), or components designed to promote tissue growth, regulatory review will lengthen. Nevertheless, if the value delivered reflects in pricing, there may be some recompense for the delay.

|

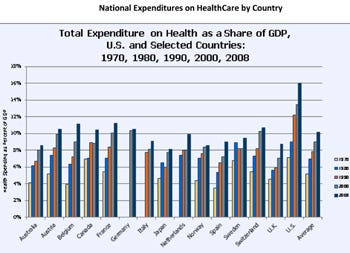

Figure 4. National expenditures on Healthcare by country. Click figure for larger image. |

The second major risk is simple: Reaching the limits of what people and countries are willing and able to spend on healthcare, with consequent controls and limitations, or behavior changes that turn patients into active shoppers for medical devices. Figure 4 shows the increase in share of gross domestic product (GDP) spent on healthcare, with the United States increasing by 10 points, from 7% in 1970 to 17.4% of GDP in 2009, the most recent year surveyed. This places the United States at the top of the world heap in share of GDP spent on healthcare; Germany, in contrast, seems able to deliver high-quality care for a substantially lower share of GDP, 10.5% in 2008, while Switzerland expends 10.6%. Even the UK, famous for its National Health Service funded from tax revenues, delivers high quality care for 8.5%. The question is, when will countries and individuals run out of the ability to pay? While it not clear exactly where the spending wall lies, it is clear that a limit is approaching.

There is also the potential for substantial consolidation in this industry, which as noted is relatively nonconcentrated at this time. The pharmaceutical industry is emerging from a series of mergers that have created pharmaceutical giants; and consolidation has occurred in many other industries, even those with high technology, high value add products, such as computers and software. It is hard not to look at the many large- and mid-sized firms in this business, some with complementary products or geographic markets, and not see the potential for a strong period of consolidation into a few large powerhouses. An early sign of this potential is the recent offer by Danaher Corp. to buy Beckman Coulter.

The final danger lies in the prospect for low-cost products and consumables offered by businesses focused on supply chains and production efficiencies. There appears to be some potential to save on costs by moving production from

North America and Europe to countries with lower wage costs. While an individual consumer might not want to have a hip replacement from a low-cost bidder, eventually the insurance provider may start to push for lower costs for comparable quality. This substitution of lower cost alternatives has started in pharmaceuticals, where there is growing pressure to replace branded drugs coming off patent with approved generics. If medical device technologies begin to stabilize and the quality of both imported substitutes and their local regulation increases, the possibility of the perfect storm of stringent reimbursement requirements, and more competitive R&D and manufacturing landscapes could squeeze U.S. medical device industry profits. The industry sector will need to rely on its resilience, durability, creativity, and innovation to face and overcome some very challenging years ahead.

Conclusion

Across the developed world, companies developing medical devices face multiple challenges. These hurdles include increased regulatory scrutiny, more severe reimbursement requirements, global talent and innovation wars, and aggressive new procurement practices. In search of top line growth, manufacturers are all looking to Brazil, China, and India, while cutting-edge innovations are gradually moving to Germany, France, Israel, and Japan.

Today, the United States is the acknowledged world leader in medical technology, but that leadership is being challenged. In order to preserve America’s leadership, there needs to be a focused and concerted effort by industry and government to making innovation in the life sciences a top priority. In addition, the U.S. R&D structure must be sustained and enhanced. Furthermore, there needs to be a close examination of the FDA review process in order to achieve a process that is predictable, consistent, and timely similar to what European biomedical device companies experience.

The U.S. medical device industry has many groundbreaking and transformational products on the market and under development today due to a continuous focus on R&D and changing consumer needs. These companies ask the U.S. government to look out for their interests in both the domestic and overseas markets through ongoing efforts to lower tariffs, streamline and simplify regulations, and ensure a level playing field against foreign competitors based in countries throughout the world. Despite the steady growth seen in the largest medical device markets (the United States, European Union, and Japan), the most promising markets for these products are located elsewhere, including China, India, and markets in Southeast Asia and Latin America, most notably Brazil. Through bilateral and multilateral forums, the U.S. government must be ready to help the medical device sector further develop and enhance its global competitiveness and make a meaningful contribution towards improving public health worldwide.

Companies face many risks, from public policy uncertainty to regulatory pressures, and payer pressures, which in aggregate are placing unprecedented challenges on medical device innovation. It is affecting the investor sector, with funding going towards the later stage and more mature companies. Yet even with all these challenges medical device companies have a lot of potential growth ahead.

To take advantage of these potential opportunities, medical device companies take the following actions:

Emerging companies must ensure that they can survive and sustain innovation through the challenging funding climate.

Companies of all sizes will need to continue exploring ways to leverage OUS (Outside United States) markets to offset domestic challenges from emerging markets. The opportunities must offer high growth potential to European countries and provide more efficient and effective routes to launch new products and expedite early cash flow.

As companies continue to grow it will be critical for them to maintain a focus on operational efficiency and effectiveness.

Companies must realign into a consumer-centric future where providing successful outcomes is paramount. In other words, innovation that goes beyond the product to include the support services and data analytics.

Companies will be required to evaluate and potentially reinvent parts of their business models to ensure that what they are offering is what the customer wants, and that these offerings are developed as efficiently as possible.

Going forward, biomedical device companies will need to demonstrate that a particular intervention improves patient outcomes and enhances the efficiency of the healthcare system. The need to offer a complete product—including the addition of services and data as part of the complete offering and solution—exists. Real-time patient diagnostic data could prove as valuable as the newly developed medical device for some product categories. In tandem, a new device, with rich patient diagnostic data and a full array of supportive services might prove to be the key for the future success of the medical device industry.

Reference

1. A Hirschman, "The Paternity of an Index". The American Economic Review 54, no. 5 (1964): 761.

Yair Holtzman is director and global life sciences leader at WTP Advisors (White Plains, NY). Tom Figgatt, Sr., is an associate at the firm.

About the Author(s)

You May Also Like