Sign up for the QMED & MD+DI Daily newsletter.

How Medical Device Companies Can Boost Operating Performance to Improve Shareholder Value

In these tough times, medtech companies must focus on operational excellence to drive growth and profitability.

Sharad Rastogi

December 20, 2012

10 Min Read

Following an era of high growth and profitability in the medical technology industry, total shareholder returns have been declining during the past few years. This decline, combined with slower revenue growth and flatter profits, indicates a transition from a growth stage to a more mature stage of the industry’s life cycle. While many medtech companies are seeking topline growth by reassessing their capabilities, global business models, and marketing strategies, they have focused less on improving operating performance as a strategy for driving shareholder value. Yet, this may be an approach they cannot afford to overlook.

Slower growth has come amid intense pricing pressure and new mandates, such as the Affordable Care Act’s medical device excise tax, which went into effect this month. At the same time, global emphasis on controlling healthcare costs is raising questions about overuse of medical technology and driving down prices of devices, supplies, and diagnostics. This greater demand to demonstrate clinical and cost effectiveness raises the bar on medical innovation, even as talk of more stringent regulatory requirements increases uncertainty about the risk of developing new products. Boosting shareholder value in the medtech industry has never been more difficult.

Operational Excellence Drives Shareholder Value

Although not the only driver of shareholder value, operational excellence is critical for maturing industries. PwC created an operating performance index (OPI) to better understand industry trends and identify operational levers that medtech companies can pull to improve shareholder returns.a The OPI and publicly reported data obtained from S&P Capital IQ were used to analyze the operating performance of 56 global medtech companies, collectively representing nearly $200 billion in medtech revenues, during a 7-year period (2005–2011). Table I shows elements of the OPI and the annual medtech industry trend for each.

| OPI Element | Description | Annual Trend Relative |

Primary Metrics | Revenue growth rate | Annual revenue growth rate | –12% |

Operating profit | Last 12-month EBITDA margin | 2% | |

Invested capital productivity | Return on invested capital | –2% | |

Secondary Metrics | Asset productivity | Revenue/property, plant, and equipment | 2% |

Labor productivity | Revenue/employee | 8% | |

Gross margin | (Revenue – cost of goods sold)/revenue | 1% | |

SG&A effectiveness | Revenue/selling, gneera, and administrative expense | –1% | |

Inventory management | Inventory turns | –1% | |

working capital productivity | Return on working capital | –1% | |

Industry-wide trends in operating performance, 2005–2011 |

On most dimensions, operating performance in the medtech industry held relatively steady from 2005 to 2011. However, some dimensions changed notably. Average annual revenue growth rates declined at a rate of approximately 12% per year, dipping into single digits during the recession and failing to return to prerecession levels by 2011. The analysis also showed that revenue growth rates among industry leaders and laggards are beginning to converge, indicating diminishing differences between them.

The OPI revealed opportunities for improvement in invested capital productivity, inventory management, working capital productivity, and selling, general, and administrative (SG&A) spending effectiveness—all of which remained relatively flat during the study period. Other key findings of the analysis revealed the following:

Operating profits grew at an average annual rate of 2%, suggesting that medtech companies worked to manage costs and became more efficient.

Although revenue growth rates declined, R&D investment held at a fairly steady level as a percentage of revenue, resulting in a 10%-per-year downward trend in R&D impact.

Labor productivity, measured by revenue per employee, improved an average annual rate of 8%.

Asset productivity showed more modest gains of 2% per year, reflecting increased focus on efficiency.

Gross margins remained essentially flat, indicating that companies reduced cost of goods sold amid pricing pressures.

Strengths and Weaknesses by Segment

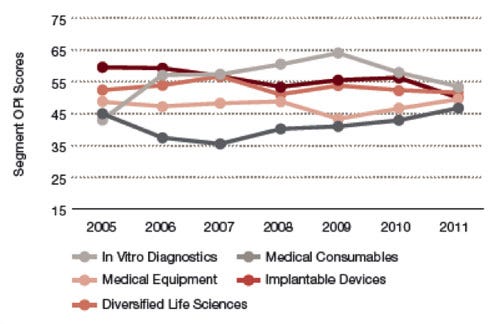

Breaking the industry analysis into segments—in vitro diagnostics (IVD), medical consumables, medical equipment, implantable devices, and diversified life sciences—revealed wide variations in operating performance.b As shown in Figure 1, the highest-performing segments were IVD, implantable devices, and diversified life sciences. The implantable devices segment led in 2005 but declined gradually, losing its edge over other segments. IVD, on the other hand, steadily improved to become one of the leading segments. The diversified life sciences segment remained fairly stable throughout the study period. Prior to the recession, medical consumables began to decline but regained lost ground by 2011. Medical equipment achieved stable operating performance prior to the recession, suffered the sharpest drop of any segment during the recession, and rebounded afterward.

|

Medtech segment OPI scores, 2005–2011. |

The implantable devices segment’s decline was likely driven by the maturation of the cardiology and orthopedic implant markets, which were both characterized by low growth, reimbursement challenges, and changes in purchasing dynamics and buyer behavior. The implantable devices segment also had the highest SG&A expenses (stemming from a high-touch sales model) and the fewest inventory turns because of its practice of maintaining large field inventory to support high service levels.

The growing importance of molecular diagnostics and personalized medicine helped the IVD segment become a leader in operating performance after 2006. Rapid operating profit gains and steady improvements in cost management and operational efficiency also boosted sector performance.

Operating performance in medical consumables showed low operating profit and low revenue growth relative to others, reflective of overall and ongoing trends in the push for value over volume.

The analysis found that medical equipment companies were hit hardest by the economic downturn. Although efficient compared with other segments’ performance, the medical equipment segment was hurt by its customers’ difficulties in accessing funds for capital investments. This problem was evident in the sharp drop in growth rates.

Conversely, the diversified life sciences segment, which includes large companies offering a diverse portfolio of medical products, remained relatively stable compared with other segments. The variation in the operating performance of these companies’ medtech units apparently was mitigated by the performance of biopharmaceutical and other business divisions.

Strategies to Improve Operating Performance

These insights into industry operating performance trends can inform specific companies about strategies for improvement. Once a company conducts its own operating performance review, business leaders can identify challenges and opportunities for improvement and decide which of the following strategies could work best.

Take a broader view of innovation. Value over volume is the mantra for the healthcare system of the future. A changing healthcare ecosystem (characterized by, for example, shifts in pricing power from device manufacturers to healthcare providers, and increasingly sophisticated customers demanding total solutions) means that medtech companies must develop new offerings catering to new ecosystem needs. In the past, innovation in the medtech industry has had a relatively narrow scope, being largely technology driven, product based, and physician focused. In the future, medtech companies will need to take a broader view of innovation. With the growing emphasis on healthcare costs and quality, areas such as clinical effectiveness, improved patient outcomes, and/or improved healthcare efficiency will become just as or more important than product innovation. In other words, Medtech players must address the needs of a broader set of stakeholders including, healthcare providers, payers, and patients, and innovate around new business models and a broader set of offerings including, products, associated services, and data or information management.

For example, some enterprising medical technology companies are securing their innovation efforts around the concept of “owning the disease” with products, services, and solutions across the continuum of care. They are adopting strategies pioneered by leading technology companies, creating innovation models anchored in consumer-centric disease solutions.

Focus on productivity. Gross margins, SG&A expense effectiveness, inventory management, and working capital productivity, have remained essentially flat over the past seven years, presenting significant opportunities for improvement. Medtech companies can adopt successful practices from other operationally efficient industries, such as high-tech, consumer electronics, automotive, and industrial technologies. For example, medtech companies can use value engineering and strategic sourcing to improve gross margins. Similar to those in other industries, medtech companies can outsource to tap external partners and capabilities and moderate development and manufacturing costs. To improve working capital and inventory management, medtech companies can more efficiently manage supply chains. They also can improve sales operations and reduce indirect expenses to drive SG&A effectiveness.

Forward-thinking medtech companies are revamping their operations to reduce business complexity and drive efficiencies by streamlining supply chains, product portfolios, supplier networks, and manufacturing and distribution footprints. Some companies are using platforming and product roadmapping approaches, similar to those of automobile manufacturers. They are designing interrelated product lines that offer differentiated products for different market segments (e.g., value, mid-range, and premium versions) and use common design, components, and manufacturing processes. This strategy allows companies to offer sophisticated products to more affluent markets but more basic devices where cost is the primary concern.

Adapt a go-to-market approach. The ongoing transformation in the healthcare ecosystem is changing the way medical devices are purchased. While buyers consolidate and gain more power, the influence of physician preference is eroding. Transparency requirements of the Physician Payment Sunshine Act are placing more scrutiny on personal contact with individual physicians. Meanwhile, healthcare delivery and payment models are evolving from fee-for-service to value-based, creating new decision-makers, different buying criteria, and greater customer diversity.

Savvy medtech companies will find opportunities to help shape new decision processes and even change the basis of competition. They will adjust sales and marketing budgets to target traditional physician customers and critical new stakeholders, including those within healthcare organizations (e.g. hospital administrators, supply chain groups, technology assessment committees), as well as patient advocacy groups, payers, and accountable care organizations. Each stakeholder requires a different value proposition and marketing approach. For example, some are best engaged through social media and mobile technology, whereas others prefer more traditional methods of communication

Explore new avenues for growth. As industry growth in developed regions slows and markets mature, developing economies present new opportunities for serving large and growing populations and accessing talent and manufacturing capabilities, often at significantly lower cost. Several leading medtech companies have established significant footprints in emerging markets. For example, some U.S.-based medtech companies have opened innovation centers in China, where internal R&D teams work with Chinese universities, research institutes, and physicians to create products tailored to local needs.

Companies also are considering a variety of other growth strategies. While traditional mergers and acquisitions are common, other creative approaches include open innovation, corporate venturing and incubation, codevelopment through partnerships, and in- and out-licensing. For example, some leading medtech companies have created corporate venturing groups to identify, fund, and accelerate the development of breakthrough opportunities. Others have established online open innovation portals to invite external product ideas and other engagement platforms to cocreate new products and solutions with external stakeholders.

Where to Begin

As the medtech industry continues to mature, individual companies may want to turn their attention inward to improve their operating performance. An OPI-based review can enable a broad evaluation to help identify significant challenges and pinpoint improvement opportunities.

The OPI can help companies establish a baseline and benchmark performance against their peers. Using the primary OPI metrics of revenue growth, operating profit, and invested capital productivity, companies can measure overall operating performance. They can use secondary OPI metrics to establish benchmarks and identify performance gaps and improvement opportunities in innovation and product development, operations and supply chain management, customer service and sales operations, and asset and labor productivity.

With an understanding of where operating performance stands most in need of improvement, management can begin digging deeper into these areas to determine what, in particular, is inhibiting better performance and where to target initiatives for change.

In an environment likely to remain difficult and uncertain, the difference between winners and losers in the medtech industry increasingly may come down to the basics of operating performance. Improving operating performance over several dimensions presents challenges. However, implementation of tailored strategies, business models, and capabilities will yield improvements that can increase shareholder value over the long term.

Sharad Rastogi is a principal in PwC’s pharmaceutical and life sciences practice. He advises medical devices/equipment, pharmaceutical, and biotechnology companies on operational strategies and execution to drive growth and improve profitability. He can be reached at [email protected].

About the Author(s)

You May Also Like

.svg?width=300&auto=webp&quality=80&disable=upscale)