Sign up for the QMED & MD+DI Daily newsletter.

As healthcare reform encourages hospitals to look more critically at what they purchase, device makers must prove their products’ worth.

May 7, 2013

16 Min Read

The hospital value analysis process for medical devices is evolving to include more formalized committees, more sophisticated metrics, and a greater influence on the procurement process. These changes are in response to pressures to contain costs and respond to U.S. healthcare reform initiatives that emphasize clinical outcomes and system efficiencies. These committees and processes have a profound influence on the technologies that will be used within their hospital and hence their commercial success. This influence is only expected to expand with the ongoing healthcare reform initiatives.

To remain competitive, medical device companies must understand the current and anticipated hospital value analysis environment and develop new processes to facilitate commercial success. This article discusses the evolution of the value analysis process and some of the strategies medical device manufacturers can use to achieve success.

History of Hospital Value Analysis

For a hospital-based medical device to be successful, physicians must want to use the device, payers must provide coverage and reimbursement, and hospitals must purchase and make the device available. In the past, physician preference primarily drove device usage. However, hospitals, like the rest of the healthcare sector, are facing increased pressure to contain costs and optimize patient outcomes. These pressures have led hospitals to create new decision-making processes to control costs. Hospital value analysis committees (VACs), also referred to as technology assessment committees, are a central feature of these decision-making processes.

If you like this story, you might also be interested in "Funding and Reimbursement: Plan Early and Often," a conference session led by Diane Francis, senior director of health economic solutions, U.S. health economics, and market access at Ethicon Inc.It takes place June 19, 2013 at MD&M East, in Philadelphia. |

VAC use has since expanded. A recent survey of more than 4,500 hospitals in the United States reported that close to three-quarters of respondents either had a strategy for standardizing physician preference items (PPI) in place or were working on one.2 The survey found that approximately 64% of hospitals were using value-analysis teams to evaluate and select PPIs and other supplies. Also, in an unpublished 2012 survey of 24 U.S. hospital stakeholders conducted by the authors, 48% of the hospitals in the sample had introduced their VAC over the past five years.3 The hospital VACs that have been in place longer (e.g., more than 10 years) have typically been restructured over time.The term value analysis committee first appeared in an article in the United States in 1977.1 Their primary goal was cost reduction, often achieved by process improvements and competitive bidding. At that time, committees were loosely comprised of materials managers, physicians, and nurses. They had informal processes that varied across hospitals. Often, the task of materials management was to distinguish between the optional versus mandatory functions and features of products. The physicians who used the products were asked general questions such as “Is the additional cost justified because of additional benefits or is the additional cost related to advertising?”1

Hospital VAC processes and their device evaluation criteria have also become more sophisticated. Whereas value analysis used to focus on product standardization and reducing costs, there is now increasing emphasis on systematically measuring and attaining quality improvement.4 Interviews with personnel in U.S. hospital materials management and supply chain roles demonstrated this message clearly by illustrating the importance of attaining a balance between cost reduction and quality improvement.

Structure and Processes of VACs

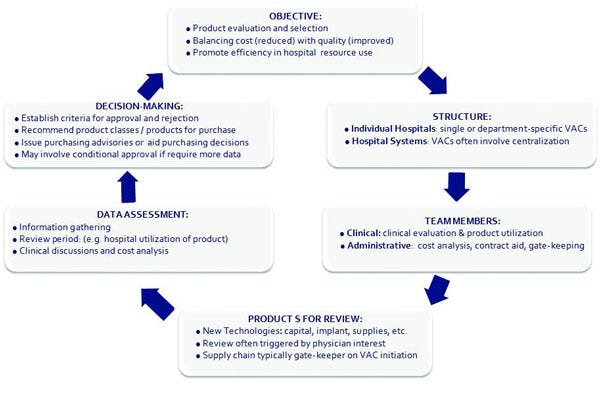

Given their focus on product evaluation to inform purchasing decisions, VACs are sometimes compared to pharmacy and therapeutics (P&T) committees, which decide which drugs will appear on the drug formulary at hospitals or insurance plans.5 Although VACs are at various stages of sophistication across the United States, they typically have several core aspects in common (Figure I).2-4, 6 Theoretically, any type of technology may undergo a VAC analysis, including capital equipment, medical devices, and supplies or disposables. However, this varies by hospital. Most VACs involve both clinical and administrative personnel, each with unique roles. Clinicians typically conduct clinical evaluation and report on product use. Administrative personnel may integrate such information with cost analysis and supplemental data review, as well as spearhead contract negotiations. Most commonly reviewed are new technologies and PPIs, which are triggered by physician interest and are anticipated to have an important financial impact. Currently used products may be reviewed upon contract renewal, for example. Supply chain personnel typically channel new product requests and determine whether value analysis is appropriate. Upon data review, VACs play a pivotal role in product selection and purchasing decisions, often using objective evaluation criteria. The level of stakeholder involvement, as well as the depth of analysis, is often more extensive for products with high budget and strategic impact.4

|

Figure I. VACs across the united states share common features.2-4,6 (Click figure to enlarge) |

Two recent, large surveys reported on the scope and challenges associated with current U.S. hospital value analysis.2,5 The surveys noted that value analysis is a common process and has become more standardized. VACs facilitate standardization processes and decisions, and assesses the value added weighed by cost. However, substantial functional variation exists in VACs across hospitals in aspects such as the level of physician involvement, regularity of meetings, and involvement of group purchasing organizations. Less than half of VACs have physicians on panel but the trend is that their involvement is increasing as more hospitals move towards a staffed-physician model. Both surveys reported that physician buy-in and data availability for decision making were key challenges impacting the function of VACs. Physician participation in VAC processes may be limited due to their availability and resistance to choice restrictions. Also, data are often limited for medical devices. Factors such as rapid device life cycles, methodological challenges in conducting randomized controlled trials (RCTs), minimal data requirements for 510(k) regulatory clearance, and difficulty with comparing all relevant competitors in one study limit the quality and quantity of data available for appropriate decision-making.6 The surveys further noted that it is difficult to assess product performance within hospitals. Although identified as challenges, physician availability and adequate data are critical to the validity of the process and to optimizing the efficiency gained with implementation.

Value Analysis in Context of Evolving Healthcare Reform

Healthcare reform is contributing to the surge of value analysis use within U.S. hospitals and the redefinition of value analysis practices. In addition to the goal of reducing the uninsured rate, an important objective of healthcare reform is to reduce inefficiencies in the healthcare system. Several healthcare reform initiatives are aimed at incentivizing hospitals and physicians to improve the quality and efficiency of care, often through performance-based rewards and penalties beyond the initial hospital episode (Table I).6

Table 1. Example health reform initiatives targeted to cut costs and improve quality and efficiency in hospitals. 6 |

Value-Based Purchasing |

Pay for Performance |

Hospital or Physician Bundled Payments |

Medicare Cuts ot Hospital-Related Programs |

Reduced Payments for Readmissions |

Capitation |

Comparative Effectiveness Research |

Accountable Care Organizations |

As an example, the accountable care organization (ACO) plan is among the first initiatives being implemented under the Affordable Care Act.6 Its aim is to provide better patient care, better health for populations, and slower growth in costs. ACOs involve networks of healthcare providers, including hospitals, physicians, post-acute care facilities, and other providers, who agree to be accountable for the quality, cost, and care of Medicare beneficiaries throughout the continuum of their healthcare needs. The task of these providers is to meet performance standards involving outcomes, patient experience, and use of services. Providers share savings if per capita expenditures are below a specified threshold. Under some models, providers face penalties if they do not meet performance standards or savings benchmarks.

Healthcare reform initiatives, such as ACOs, are expected to have a significant effect on hospitals and VACs. Such initiatives will expand the focus of VACs from reducing product costs to reducing resource use and improving patient outcomes across a broader spectrum. This approach results in systems and analyses that resemble those used for managed care organizations and single-payer systems, where longer-terms outcomes and resource use are considered in product selection. The new focus will require a greater reliance on evidence-based approaches to product assessment, including comparative effectiveness, health technology assessment, and health economic methods.

Recent reports provide some evidence of this shift, which is only expected to become more apparent.2,5,7 The Journal of Healthcare Contracting published findings of interviews with several senior personnel in U.S. hospital materials management and supply chain positions. The largest anticipated changes in healthcare contracting over the next several years were aligned with healthcare reform initiatives:7

Ongoing and increasing demand for cost reductions and savings.

A need for better tools for evaluating and weighing clinical benefits versus device cost.

Increasing expertise among supply chain managers, resulting in enhanced cost analysis.

An increase in physician involvement and collaboration in contracting and cost reduction.

Patient focus, where companies strive to address added value in product development.

Materials management serving a vital role as organizations try to optimize cost versus quality.

More contracts with value-enhancement clauses tied to patient outcomes.

Increasing demand for evidence showing incremental improvement stakeholders are willing to pay for.

Strategies for Device Manufacturers to Meet VAC Needs

Medical device manufacturers that understand and respond to the current and evolving role of VACs will have a market advantage. It will be essential for manufacturers to understand the VAC process and future direction, identify and quantify the entire product value proposition, provide evidence for value assessment, and create systems to optimally communicate with VAC stakeholders.

Understand the VAC Process and Future Direction. The first step is to understand how VACs function and make decisions. Manufacturers should aim to gather details of VAC processes for key hospital accounts. Key information to obtain includes the following:

VAC membership composition.

Decision processes.

Metrics used to evaluate products.

Factors outside of hospital care that may influence decisions.

Opportunities for formal and informal presentation of data and product value proposition.

Opportunities for formal and informal dialogue with VAC members.

The process of gathering information must be ongoing, as healthcare reform initiatives are expected to create new pressures, requirements, and opportunities for VAC use.

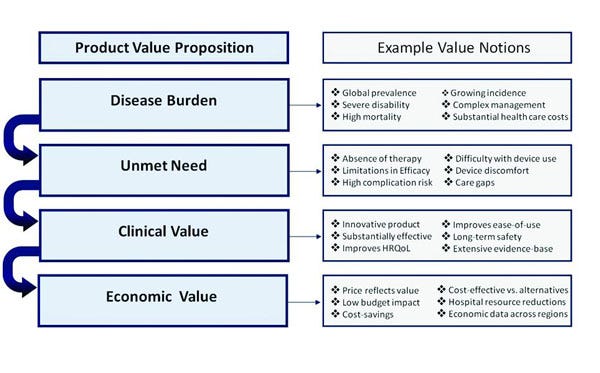

Identify and Quantify the Entire Product Value Proposition. Hospitals are increasingly adopting evidence-based evaluation of medical devices to characterize product value not only in terms of clinical benefits, but also other patient, process, and cost-related outcomes.6 As discussed, the ACO initiative may increase this focus and expand it to outpatient as well as inpatient outcomes. Due to this evidence-based, broad focus, manufacturers will benefit from presenting comprehensive value propositions. Figure II provides a framework for elements in a value proposition that can be used to communicate the value of medical devices.

|

Figure II. Medical device manufacturers can use this framework for a product value proposition to communicate the value of medical devices.6(Click figure to enlarge) |

Consideration of the entire value proposition should begin early in the product life cycle. Manufacturers must consider whether expected product value will be acceptable to payers and hospital purchasers, as well as what types of studies are required to maximize the perceived value of the product. Early strategic assessments can help inform whether the device is a good candidate for further development. Evidence-generation plans should encompass a range of study designs and objectives, such as traditional randomized trials, comparative effectiveness research, studies focusing on patient-reported outcomes (e.g., HRQoL), long-term safety and effectiveness assessment in real-world populations, burden of disease studies, cost-effectiveness evaluations, and budget-impact analyses from hospital and payer perspectives.6

Manufacturers must also consider price in relation to the product value proposition, in addition to other market and financial factors. Such preparation will help avoid aggressive rebates to achieve sales. Finally, ongoing evidence generation is essential to continuously demonstrate the clinical and economic advantages of the medical device versus the most relevant alternatives, and to sustain product price and reimbursement after launch.

Provide Evidence for Value Assessment. Many studies evaluating hospital VACs in the United States have identified limited data on comparative effectiveness and cost impact as the central challenge. Hospitals are also challenged with linking products with hospital-based outcomes. Decision-making is typically informed by literature review, physician guidance and hospital experience, third-party reports, and data provided by vendors.3 However, these sources may be incomplete, of poor quality, or associated with perceived vendor bias. In some instances, hospitals may delay the decision to purchase a product until further evidence is generated. This data gap provides an opportunity for the device industry to play a leadership role in high-quality data generation. Such data will allow manufacturers to fully convey the value proposition of their medical devices.

For manufacturers to develop high-quality, unbiased data that suits the objectives of hospital value analysis, the following is recommended:

Maximize the credibility of data through use of appropriate methodologies, unbiased opinion leader involvement, and peer-reviewed publication.

Measure real-world performance of technologies (e.g., registries) to help fill information gaps. Such information is often missing or inadequate and can delay product uptake.5,8 Observational data may not answer all types of questions (e.g., comparing device efficacy), but it may be essential for determining long-term performance and safety in larger, real-world populations.8

Collect data on outcomes that matter to hospitals from a cost-efficiency standpoint, such as reduced hospital-acquired infection, blood loss, hospital stay, procedure time, and re-admissions, in addition to improved clinical outcomes.

Quantify hospital-related cost reductions through comprehensive budget-impact analyses.

Develop comprehensive, methodologically sound, and adaptable tools to communicate clinical and economic product value. Tailoring analyses to hospital-specific parameters and informing them with high-quality data, will increase applicability and acceptance of such tools in the hospital.

Ensure data are timely (e.g., considers all relevant comparators on the market using indirect comparisons), so they are relevant to decision-making.

Support VAC reevaluation processes through ongoing data generation in the hospital (i.e., link product with outcomes).

Create Systems to Optimally Communicate with VAC Stakeholders. Manufacturers have several potential points of contact with stakeholders that may be involved in the VAC process. These include physician training and education, product trial periods, and contract negotiations. Through these interactions, manufacturers should maximize opportunities to communicate product value and supporting evidence. Recent studies have noted that it is not yet clear how the relationship between physicians and vendors may be affected by more aggressive standardization efforts.5 However, it is generally predicted that hospitals will increasingly limit traditional sales interactions to those that are perceived to be most valuable (e.g., training on products physicians are unfamiliar with). Maintaining an appropriate balance between serving vendor versus physician goals will be essential to achieve success.

In addition, the new economic stakeholders will require more complex models. These include different sales approaches, involving provision of more sophisticated data (e.g., comparative effectiveness, outcomes research and budget impact), outcomes-based contracts, and bundled purchasing models.6 Scientific channels of communication, beyond traditional sales and marketing, may be required. Together, these personnel should aim to excel in increasingly complex contract negotiations that focus on solutions and outcomes. They must anticipate evolving needs (e.g., value demonstration beyond efficacy), extend product offerings beyond price alone (e.g., bundling, risk-sharing), and respond rapidly and efficiently to concerns (e.g., data queries, evidence generation).

Conclusion

Hospital VAC use has increased and processes have expanded over time. VACs are increasingly focused on attaining an optimal balance between cost reduction and quality improvement. Most VAC structures include both clinical and administrative personnel to conduct clinical evaluation and provide cost analysis information and data review. However, there are several challenges associated with current U.S. hospital value analysis including physician buy-in and data availability. Healthcare reform has contributed to the surge in hospital value analysis as several initiatives are aimed at incentives for hospitals and physicians to improve the quality and efficiency of care. As a result, there is an evident shift towards increased use of VAC in hospital settings. It is thus essential for medical device manufacturers to understand the VAC process, identify and quantify their product’s clinical and economic value proposition, provide evidence for value assessment considering outcomes that are relevant to hospital settings, and create systems to optimally communicate with VAC stakeholders.

References

1. L. Boegradine, "Committees ensure cost efficiency in purchasing," Materials Management, 51 (1977): 133–136.

2. G. Aston, S. Hoppszallern, "Preference matters," Hospital and Health Networks, October (2009).

3. P. Ehrhardt, R. Saadi, "Assessment of Hospital Value Analysis Committees," (unpublished survey results) 2012.

4. R. Barlow, "Redefining value analysis practices for a healthcare reform-minded industry," Healthcare Purchasing News, October (2009).

5. K. Montgomery, E.S. Schneller, "Hospitals’ strategies for orchestrating selection of physician preference items," Milbank Quarterly 85, no. 2 (2007): 307–335.

6. R. Saadi, D. Grima, N. Ferko, The Science of Commerce: Succeeding in the Changed Medical Device Market. (New Jersey: ECON Publishing, 2012).

7. "Top Ten People to Watch," Journal of Healthcare Contracting, 2009, 2010, 2011.

8. Physician-Hospital Alignment in Device Selection: Roundtable Summary, [online] (Berkeley, CA: Integrated Healthcare Association and the Berkeley Center for Health Technology, October 2, 2009); available from Internet.

Ryan Saadi, MD, MPH, was formerly global vice president of health economics, reimbursement, strategic pricing, and market access at Cordis Corp., a Johnson & Johnson company.

Nicole C. Ferko, MSc, is a director at Cornerstone Research Group (Burlington, ON, Canada).

Peter Ehrhardt, MBA, is a partner with Simon-Kucher & Partners (Cambridge, MA).

Daniel T. Grima, MSc, is a partner with Cornerstone Research Group.

Related Content

The New Commerce: How Sales Models are Changing in Medical Devices

In the New Medical Device Sales Model, Managers, not Reps, Need Better Training

Medical Device Sales Poaching: Should You Be Concerned?

Tracking Reimbursement and Payment Trends

New IVD-Reimbursement Bill Introduced on Capitol Hill

You May Also Like