Sign up for the QMED & MD+DI Daily newsletter.

The medical device sector experienced unprecedented growth in revenue and earnings over the last decade. While sales and profits in most industries lagged due to worldwide recessions, medtech companies rewarded their investors with handsome returns. Long viewed as the smaller sibling to Big Pharma, the medtech industry now generates more than $200 billion in annual revenue worldwide, excluding sales of diagnostics.1 The U.S. market accounts for nearly half of the global market, with projected sales of $95 billion in 2010.2

Kevin O’Keeffe

June 10, 2011

38 Min Read

The medical device sector experienced unprecedented growth in revenue and earnings over the last decade. While sales and profits in most industries lagged due to worldwide recessions, medtech companies rewarded their investors with handsome returns.

Long viewed as the smaller sibling to Big Pharma, the medtech industry now generates more than $200 billion in annual revenue worldwide, excluding sales of diagnostics.1 The U.S. market accounts for nearly half of the global market, with projected sales of $95 billion in 2010.2

Long viewed as the smaller sibling to Big Pharma, the medtech industry now generates more than $200 billion in annual revenue worldwide, excluding sales of diagnostics.1 The U.S. market accounts for nearly half of the global market, with projected sales of $95 billion in 2010.2

The medical device market encompasses a range of subindustries, including product areas such as cardiovascular and orthopedic devices, woundcare products, disposable supplies, and durable equipment. The cardiovascular and orthopedic segments represent approximately 35% of the worldwide market, with annual sales of $37 billion and $33 billion, respectively.3–4

Over the past 10 years, there has been a sea change in the role of devices sin the healthcare marketplace. Diversified companies that once relied on pharma to bolster their earnings began looking to devices for sustained growth. For instance, consider the revenue and margin mix for healthcare giants Johnson & Johnson (J&J) and Abbott. In 2000, 62% of J&J’s consolidated operating margin was generated by pharma, while 25% was generated by devices. By 2009, the two had changed places, with devices driving 46% of consolidated operating margin and pharma driving 39%. The story at Abbott is similar, but the numbers are still playing out. Overall, sales from 2004 to 2009 grew by 56%, but pharma revenues grew by 38% over that period.5 Much of Abbott’s recent growth has been fueled by its once-immaterial vascular device business, which emerged from its 2006 acquisition of Guidant’s vascular business.

|

|---|

Figure 1. The image above compares the return on a $100 investment. |

The medical device industry has been treating investors well. Case in point: Had a savvy financier invested $100 in the S&P 500 Medical Equipment Index on New Year’s Eve in 1999, that investment would have been worth $173 on December 31, 2009—a 6% annualized return. Had he invested in the S&P 500 Pharmaceuticals Index, the investment would have been worth just $83—a 2% annualized loss.6

These returns tell a consistent story: The medical device industry has outperformed the pharmaceutical industry for the past decade in terms of revenue growth. The question that remains is whether medical device companies and their investors will continue to prosper.

Barriers to Innovation

The medical device industry has its share of concerns, most of which have been brought on by impending healthcare reform. In March 2010, the House of Representatives passed healthcare legislation that included a 2.3% tax on medical device revenue, which will go into effect in 2013. The tax is broad in scope and will be levied on all medical device companies regardless of revenue and profit.

Perhaps more threatening is the discussion of additional reform that could require medical device companies to provide FDA and insurance companies with evidence of comparative effectiveness. Healthcare reform included the development of the Patient-Centered Outcome Research Institute, an advisory panel that will conduct and disseminate comparative effectiveness research. The research is funded by $1.1 billion set aside under the American Recovery and Reinvestment Act of 2009. Medical device manufacturers worry that studies on comparative effectiveness may soon become an integral part of clinical trials, adding time and expense to medical device development.

|

|---|

Figure 2. Shown here is one new molecular entity and biological license application approvals. |

Despite these concerns, the medtech sector still holds great promise. A close look at regulatory trends for medical devices compared with pharmaceuticals demonstrates that medtech entrepreneurs are still more likely to realize return on their investment than their pharmaceutical counterparts. Although few medical devices can produce the kind of sales that blockbuster drugs are known for, devices require less development risk and are easier to bring to market than pharmaceuticals.

The drug-development process requires significant investment in time and resources, taking 10–15 years for an experimental drug to travel from lab to patient at an average cost of $1.3 billion.7 Characterizing the development process for a new medical device is more difficult. The process is likely to begin with a single inventor or a small development-stage research company. The process from prototype through preclinical animal testing can take two to seven years, often costing anywhere from $50 to $100 million.8

In the United States, devices are assigned to one of three classes by FDA before gaining clearance to market. The class to which a device is assigned determines the type of FDA submission required for clearance to market.

Class I devices are simpler than Class II/III devices and are subject only to general controls. These devices are generally non-life-supporting. Most Class I devices do not require FDA review.

Class II devices are slightly higher risk than Class I devices and require special controls, including performance standards, design controls, and post-market surveillance. Most Class II devices only require 510(k) approval, a process that allows FDA to determine whether the device is equivalent to a device already placed into one of the three classification categories.

Class III devices are generally characterized as life-sustaining devices, and include pacemakers and drug-eluting stents. These devices require special controls and often require premarket approval (PMA), an FDA submission process involving large clinical trials to evaluate the safety and effectiveness of the device.

Development of a new Class III device, such as a novel drug-eluting stent, often requires preclinical trials, pilot studies, and a pivotal trial. Pilot studies often involve fewer than 100 patients treated at a few centers. The goal is to establish safety and efficacy within a target population. Pivotal studies for new Class III devices can require enrollment of more than 1000 patients at 30–50 sites over a period of one to two years. The cost of a pivotal trial for a new device can vary. As a baseline example, an 800-patient multicenter, randomized trial for a Class II guidewire was estimated to cost $10 million to $12 million over a 24-month period.9 A larger trial for a Class III device could cost much more.

Overall, the regulatory process for a new Class III device could take five years from prototype to PMA approval and could cost $50 million to $100 million.10 In contrast, experts cite clinical trials for new pharmaceuticals, which exceed $100 million with Phase 3 trials and can cost upward of $25,000 per patient.11–12 Further, industry experts claim that medical devices have an average development cycle of just 18 months, compared with 120 months for pharmaceuticals.13

The regulatory pathway for pharmaceuticals has also become increasingly challenging. Only five in 5000 compounds entering preclinical testing will make it to human testing, and only one of those five will be approved for sale.7 The rate at which FDA’s Center for Drug Evaluation and Research is approving new drugs has fallen considerably over the last 15 years.13

In contrast, FDA receives thousands of medical device submissions each year, the vast majority of which are 510(k)s and PMA supplements, as opposed to original PMAs for new devices. The U.S. Government Accountability Office reports that from 2003 to 2007, FDA reviewed 13,199 submissions for Class I and II devices via the 510(k) process, clearing 11,935 (90%) of those submissions. The agency reviewed 342 submissions for Class III devices through the 510(k) process, clearing 228 (67%) of the submissions. Furthermore, it reviewed 217 original and 784 supplemental PMA submissions for Class III devices and approved 78% and 85%, respectively.14

Approval timelines and regulatory trends provide justification for continued medical device innovation. The device tax may stymie earnings and studies on comparative effectiveness may continue to worry CEOs, but investment in devices will continue to provide a less costly and more predictable alternative to investment in pharmaceuticals.

Recent Success Stories

Coronary stenting. Over the past 10 years, billions of R&D dollars were spent exploring opportunities for minimally invasive devices and interventional procedures that could replace open surgical procedures. The rapid uptake of coronary stenting for the treatment of atherosclerosis is the best example of this trend. The onset of coronary stents was widely covered in industry journals and even mainstream media outlets.

|

|---|

Figure 3. Depicted here is FDA device submissions, approvals and denials in 2008. |

Bare metal stents were first introduced in the United States in 1994, with FDA’s approval of J&J’s Palmaz-Schatz stent. In 1995, the Palmaz-Schatz was used in approximately 100,000 procedures in the United States. Eight years later, FDA approved the first drug-eluting stent, J&J’s Cypher Stent. And by 2006, more than 1-million stenting procedures were being performed annually in the United States, each requiring an average of 1.4 stents, resulting in a $2.5-billion market.15

As stent demand grew, so did acquisitions, licensing, and of course, litigation. The frenzy began with J&J’s takeover of the Cordis Corp., in 1995, for $1.8 billion—a transaction that gave J&J a full line of cardiovascular devices, including catheters, angioplasty balloons, and stents.

The most notable transaction in the race to capture stent market share was Boston Scientific’s acquisition of Guidant Corp., a manufacturer of pacemakers, defibrillators, and vascular intervention devices, including stents. Guidant’s stockholders initially approved a $25 billion takeover by J&J in 2004. However, subsequent Guidant product recalls caused J&J to lower its bid by 15%. Soon thereafter, Boston Scientific entered an unsolicited bid for Guidant, and a bidding war broke out between Boston Scientific and J&J. Boston Scientific ultimately acquired Guidant, in 2006, for $27.3 billion, a price that many speculators thought was too rich, at more than 50 times the earnings.16

As part of the acquisition, Boston Scientific divested Guidant’s vascular business to Abbott Labs to alleviate antitrust concerns. Guidant’s vascular business included the already-popular Rapid Fire stent delivery system and its promising Xience V stent that was still in development. The Xience V has since become the best-selling stent in the world, with 54% worldwide market share and 58% U.S. market share.17

Stent transactions carried over into the courtroom, with patent licensing disputes between J&J and Boston Scientific, among others, playing out for almost 10 years. In February 2010, Boston Scientific announced it would pay $1.725 billion to J&J to settle these long-running patent disputes. The settlement marks the largest sum ever paid to resolve a patent litigation over a medical device. Further, the settlement followed another payment of $716 million by Boston Scientific to J&J in accordance with other stent patent litigation.18

Future innovation in the market for interventional cardiology devices used to treat coronary artery disease is expected to come in the form of bioabsorbable stents and drug-eluting balloons. Bioabsorbable stents will eventually break down into the patient’s blood stream, thereby eliminating the need for dual antiplatelet therapies (aspirin or clopidogrel) following a stenting procedure. Antiplatelets are currently used to prevent late stent thrombosis, a potentially dangerous complication whereby blood clots form inside the stent. Late stent thrombosis affects less than 1% of patients but is still considered a highly dangerous complication than can lead to death.19 Abbott’s bioabsorbable vascular scaffold is the farthest along in development and is currently being tested in Abbott’s Absorb trial. Bioasorbable Therapeutics, Biotronik, and REVA Medical are also developing bioabsorbable stents.

Drug-eluting balloons are expected to make inroads in the treatment of small vessels that are difficult to reach with stents and in-stent restenosis (ISR), the growth of tissue inside an existing stent that causes a renarrowing of the artery. Although drug-eluting stents elute antiproliferative agents intended to prevent such tissue growth, ISR remains a common complication often requiring subsequent reintervention. Interventional cardiologists often treat ISR by introducing an additional stent inside the occluded stent. Drug-eluting angioplasty balloons are thought to be a potential alternative to treating ISR, whereby additional antiproliferative agent would be transferred from the surface of the angioplasty balloon to the tissue growing inside the existing stent. Alternatively, drug-eluting balloons could be used to treat occlusions in smaller vessels that are difficult to cross with a stent. Primary competitors researching drug-eluting balloons include Medtronic, B. Braun, Aachen Resonance, and EuroCor—each of which has obtained CE Mark approval for the treatment of small vessel disease and ISR in Europe.

Robotic surgery. Another example of a new device transforming the standard of care and creating a billion-dollar market in the process is Intuitive Surgical’s da Vinci robot. The da Vinci enables surgeons to perform minimally invasive endoscopic surgery from a remote computer console while viewing the surgical field from a monitor. The robot translates the surgeon’s hand movements, which are performed on instrument controls at the console, into corresponding micromovements of instruments positioned inside the patient through small incisions.

FDA’s approval of Intuitive’s da Vinci robot was granted for performing prostatectomy procedures in May 2001. Today, about 80%–90% of the roughly 100,000 radical prostatectomies performed in the United States per year are performed robotically.20 Hysterectomies, the most commonly performed gynecologic surgical procedure, are also transitioning to robotic procedures. FDA approved the da Vinci robot for use in those procedures in April 2005. Intuitive estimates that 69,000 hysterectomies were performed using a da Vinci robot in 2009, approximately 13% of the 600,000 procedures performed in the United States each year.21

With little or no competition from new entrants in the field of robotic surgery, Intuitive’s revenue grew at a 59% compound annual growth rate from 2001 to 2009. Intuitive’s sales and marketing strategy is based on an annuity-like business model. Once a hospital purchases a da Vinci robot, a continuous supply of instruments is purchased on a regular basis. The systems are also serviced regularly. The average price for a new system is $1.4 million, and average recurring revenue of instruments and service per installed system amounts to $430,000 per year.22 In 2009, eight years after its initial FDA approval, Intuitive’s revenue topped $1 billion.23

While no competitors have emerged with robotic surgery systems that will compete directly with Intuitive Surgical’s FDA-approved indications, competitors focusing on other indications are emerging. One such competitor is Corindus Vascular Robotics, an early-stage company designing a robotic surgery system for use in percutaneous coronary interventions. In the United States, approximately 1.1 million percutaneous coronary interventions are performed each year.24 The company was granted conditional investigational device approval by FDA in January 2011 to evaluate the safety and effectiveness of its CorPath 200 System in delivering and manipulating guidewires and stent/balloon systems. The CorPath Precise pivotal trial is a prospective, single-arm, multicenter study that will enroll 154 patients.

Hansen Medical, which was led by former Intuitive Surgical founder and chief executive Frederic Moll, MD, until 2010, is developing a robotic catheter for the treatment of atrial fibrillation. Atrial fibrillation affects more than 3.3 million people in the United States and 4.5 million in Europe. The company received conditional investigational device approval from FDA to review the safety and efficacy of the Sensei X Robotic Catheter System in May 2010. The Artisan trial is a prospective, randomized study of the Sensei X System for introducing the Biosense Webster (owned by J&J) Thermocool catheter in patients with atrial fibrillation. The study has two arms and will enroll 300 subjects at 14 sites worldwide.25

Coronary stents and robotic surgery are only two examples of medtech markets that have witnessed tremendous innovation and growth over the past decade. Other success stories are looming, many of which are based on devices used in minimally invasive surgical procedures. Transcatheter heart valves and peripheral stents are at the top of the list, seeking to fill enormous unmet need in their respective markets.

Expected Areas of Future Growth

Percutaneous heart valves—aortic valves. The U.S. market for cardiac surgery devices is estimated at $1.5 billion to $2.0 billion annually, with some analysts calling for the market to reach $3.7 billion by 2015.26 The market includes heart valves, coronary artery bypass grafting devices, cardiac assist devices, and heart closure devices.

The onset of transcatheter heart valves, also known as percutaneous heart valves, represents the largest developing opportunity within the cardiac surgery device market and could potentially expand the market well beyond current estimates. Percutaneous valves are expected to replace at least some of the mechanical and tissue heart valves currently implanted using open surgical procedures. These devices are also predicted to expand the patient population eligible for heart-valve surgery, opening up valve procedures to less-stable patients considered high-risk for open heart surgery.

Transcatheter heart valves are another example of the movement toward minimally invasive technologies. Most percutaneous valve procedures require no chest incision, which is a significant advancement over open-heart surgery for many reasons. Most notable is a drastically improved experience for the patient. Open-heart surgery for valve replacement typically takes 4–6 hours and is followed by two to three months of recovery, whereas percutaneous valve procedures typically take 90 minutes and are followed by a few days of recovery.27

Percutaneous aortic valve replacement (PAVR) allows a synthetic valve to be transported to the heart via a transfemoral catheter inserted in the patient’s leg. PAVR is performed to treat aortic valve stenosis (AVS), the most common valve abnormality in the United States. AVS affects an estimated 2.5 million people, most of whom are over 60 years old. Some estimate that as many as one-third to one-half of these patients are not referred for surgery because they are considered high-risk.28 The heart’s aortic valve controls blood flow from the left ventricle into the aorta, then through the rest of the body. AVS occurs when the heart’s aortic valve begins to narrow, thereby obstructing blood flow. AVS can result in congestive heart failure and fainting.

Edwards LifeSciences and Medtronic are leading the way in the development and commercialization of PAVR technology. Edwards received a CE Mark for its Sapien valve in September 2007 and its next-generation Sapien XT valve in March 2010.29 Both products are currently being sold in Europe, with sales expected to top $200 million in 2010.30–31 In 2007, FDA awarded Edwards an investigational device exemption (IDE) in the United States for its Sapien product, allowing Edwards to begin enrolling patients in its Partner pivotal trial that is expected to lead to FDA approval some time in 2011.32 Edwards has filed for an IDE for its Sapien XT Partner II pivotal trial.

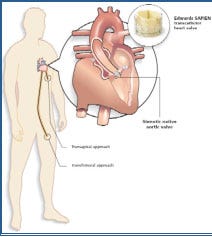

Edwards is the only manufacturer PAVR technology that can be implanted via transfemoral or transapical approaches. Edwards cites this as an important distinction that will allow cardiac surgeons and interventional cardiologists to use its technology. In the transfemoral approach, the valve is delivered via a catheter placed in the patient’s leg. The transapical approach involves a minimally invasive surgical procedure that requires a small incision between the ribs to access part of the heart. The valve is then delivered using a special delivery system.

Medtronic’s PAVR technology is three to four years behind Edwards’ in the United States. In 2009, Medtronic acquired CoreValve and its ReValving System for $700 million, and then subsequently acquired Ventor Technologies, which makes transcatheter delivery systems, for $325 million. CoreValve received CE Mark approval for its ReValving System in May 2007.33 Medtronic recently received IDE approval for a pivotal clinical trial in the United States, but FDA approval of the ReValving System is not expected until three to four years after the Edwards Sapien valve reaches market.32 The Medtronic CoreValve ReValving System has experienced great success in Europe and is currently being used in 75% of transfemoral percutaneous valve replacement procedures.34

In January 2011, Sorin Medical received CE Mark approval for its self-anchoring aortic heart valve, Perceval S. The valve is a suture-less biologic valve delivered transapically that allows the surgeon to replace the diseased valve without suturing the new valve into place. The system has been implanted in more than 10,000 patients. Sorin expects to make the valve immediately available for commercial use in Europe.35

Reimbursement permitting, PAVR could become the gold standard for aortic valve replacement and repair. Early clinical trial results are promising. Results from Edwards’ Partner pivotal clinical trial were released in September 2010, demonstrating that the Sapien aortic valve met the primary endpoints of all-cause mortality and mortality plus repeat hospitalization. The Partner trial demonstrated that transcatheter aortic valve implantation (TAVI) reduces death in patients with severe aortic stenosis who were not suitable candidates for surgery as compared with standard therapy. All-cause death was 20% lower within the TAVI cohort.36

At least 16 other companies also have percutaneous aortic valve technologies in development. Current competitors estimate that the global market for percutaneous aortic valves could reach $2.5 billion by 2014.37 Edwards expects its first four quarters of sales in the United States following launch to reach $150 million to $250 million.38

Percutaneous heart valves—mitral valves. Industry experts suggest that the percutaneous mitral valve market has the potential to surpass the percutaneous aortic market in terms of procedures and revenues.41 However, the percutaneous mitral valve market is still earlier in development and may ultimately require several valve approaches, including both mitral valve repair and mitral valve replacement. The mitral valve is located on the left side of the heart and controls blood flow from the left atrium into the left ventricle. When the mitral valve’s leaflets fail to create a tight seal, blood begins to flow backward into the left atrium. This is called mitral regurgitation (MR). MR puts an added burden on the left ventricle and lungs and may cause stroke, congestive heart failure, irregular heartbeat, or sudden death.

MR is the most common type of heart insufficiency in the United States, affecting approximately 4 million people, with annual incidence of 250,000. Only about 50,000 people are currently treated each year.40

In 2009, Abbott acquired Evalve Inc., the market leader in percutanteous mitral valve repair, for $320 million plus $90 million in milestone payments. Guidant was an early investor in Evalve. Therefore, Abbott held an interest in Evalve prior to the acquisition as a result of acquiring Guidant’s vascular business.40 The Evalve MitraClip device focuses on repairing the mitral valve. The MitraClip received a CE Mark in Europe in 2008 and subsequently received IDE approval by FDA to begin its Everest II pivotal clinical trial in the United States. Abbott anticipates FDA approval of the MitraClip device in 2011.41

Cardiac Dimensions’ Carillon Mitral Contour System received a CE Mark in January 2009. The Carillon implant consists of a shaping ribbon between distal and proximal anchors. It is delivered percutaneously via jugular vein access and is designed to be positioned, adjusted, and gently anchored in the coronary sinus and great cardiac vein to reshape the annulus around the mitral valve. An important feature of the device is its ability to be recaptured at the time of procedure, if necessary.

MiCardia’s enCor Mitral Valve Repair System received CE Mark approval in November 2010. The enCor system focuses on mitral valve repair and can adjust the mitral valve annulus to correct residual mitral valve regurgitation.

Edwards, once a key competitor in the development of mitral valve technology, decided to discontinue its mitral valve program due to slow enrollment in clinical trials. The company’s Monarc mitral valve repair device is no longer under development.

Early clinical trial results in the mitral valve repair space have been promising. Abbott’s Everest II trial investigating use of the Mitraclip device for mitral valve repair met both safety and efficacy endpoints. The Mitraclip device demonstrated a superior safety profile to surgical repair, with 9.6% of MitraClip patients and 57.0% of surgery patients experiencing a major adverse event at 30 days. In the primary effectiveness endpoint, the MitraClip device was non-inferior to surgery at one year, with a clinical success rate of 72.4% for MitraClip patients as compared with 87.8% for surgery patients.40

At least nine other companies are also developing percutaneous mitral valve technologies, some focusing on repair and others focusing on replacement. The potential U.S. market opportunity for percutaneous mitral valve technology is estimated to be at least $2 billion.

Industry analysts speculate that continued positive clinical trial results in the aortic and mitral space could drive acquisitions in 2011. Large device companies such as J&J and Boston Scientific have not publicly discussed their strategy for competing in the percutaneous valve space, leading many to believe they are waiting to see which technologies can demonstrate the most potential for commercial success.42

Peripheral stents and drug-coated angioplasty balloons. The treatment of peripheral vascular disease (PVD) is another area poised for growth in the coming years. PVD is characterized by the development of plaque and fatty deposits that lead to occlusion of the arteries in the lower extremities, typically the superficial femoral artery (SFA) or the tibial arteries. Occlusion of the SFA and tibial arteries leads to critical limb ischemia (CLI), a severe obstruction of blood flow to the hands, legs, and feet.

PVD affects eight million people in the United States and is most prevalent among diabetics and African-Americans, particularly those over age 65. Approximately 12–20% of Americans over age 65 are affected by PVD, but only 25% of those seek treatment.45, 49 Incidence is growing at 5–10% per year as a result of an increasing diabetic population and an overall increase in the senior population.46

Left untreated, PVD can result in CLI, which is associated with severe pain, significant risk of limb amputation, and mortality. The symptoms of PVD are difficult to detect, often resulting in diagnosis at a relatively advanced stage. Approximately 30% of patients diagnosed with PVD die within two years, and 12% lose a limb to amputation within three months.47 Studies report that PVD patients who develop CLI have a one-year mortality and amputation rate that exceeds 50%.48 PVD is also considered a marker for cardiovascular disease and is associated with an elevated risk for heart attack and stroke. People with PVD are four to five times more likely to die from a cardiovascular event than those who do not have the disease.49

Treatment options for patients with PVD are limited, and few options have demonstrated sustained improvement in vascular patency. Patients with less severe disease are often treated with dietary changes and drugs that help improve blood flow, typically antiplatelet drugs such as aspirin and anticoagulant drugs such as heparin and warfarin. Cholesterol lowering drugs that reduce the body’s development of fatty deposits and plaque are also common therapies.

Severe cases of PVD are often treated with surgical procedures such as endarterectomy, grafting, or bypass. In endarterectomy procedures, vascular surgeons clear plaque from the diseased arteries using a variety of surgical instruments. In grafting and bypass surgery, the surgeon replaces the diseased artery or channels blood around the blockage.

Complication rates and the invasive nature of surgical procedures have led to an increase in endovascular procedures, such as balloon angioplasty, stenting, and atherectomy for the treatment of PVD. Endovascular procedures for the treatment of PVD in the SFA have become increasingly common, with numerous clinical trials focusing on the use of stents and angioplasty balloons as an effective means of revascularization. The treatment of PVD for tibial occlusions remains less explored, and outcomes for patients with severe tibial occlusions are often more bleak.

Endovascular products have yet to demonstrate significant improvement in patient outcomes, but large medical device companies are convinced that drug-eluting stents and potentially drug-eluting balloons will one day change the treatment landscape for PVD patients. To date, engineers have struggled with stent architecture due to the tortuous nature of the peripheral vasculature. SFA lesions are long, extending to 20–30 cm, compared with coronary lesions that are often less than 4 cm in length.48 The lower extremities also subject a stent to more bending and twisting than is typical of the coronary arteries. As a result, clinical trials for the use of stents in the SFA have been marked by high stent-fracture rates.

Few stents have been FDA approved with indications for use in the SFA, and no stents have been approved for use in below-the-knee (tibial) procedures. Early clinical trials examining the use of bare-metal and drug-eluting stents in the SFA showed little difference in patency outcomes. For example, the Cordis (J&J) Sirocco trial studied the use of the Cordis sirolimus-coated, self-expanding nitinol stent against the same stent without drug coating. Both the drug-eluting stent cohort and the bare-metal stent cohort demonstrated in-stent restenosis of 21–23% at 24 months. Cordis concluded that the results did not show any significant difference between the two stents. Stent fracture also proved problematic, with approximately 20% of patients showing signs of fractures at 24 months.49

|

|---|

Figure 4. Intuitive surgical revenue and installed system base is shown. |

Bard’s bare metal LifeStent carries an FDA indication for use in the SFA. Bard’s Resilient pivotal trial demonstrated freedom from target vessel revascularization (an additional percutaneous intervention resulting from restenosis) at 12 months of 83.2% for the LifeStent, compared with 46.2% for patients who received balloon angioplasty procedures.50 Two-year data showed freedom from target lesion revascularization of 78% for the LifeStent versus 42% for the angioplasty cohort.51 Accordingly, clinical data has demonstrated some benefit to stenting when used in place of traditional angioplasty.

The Resilient trial also showed improvements in stent fracture rates compared with the results of the Sirocco trial. Of 287 implanted stents, only 11 (3.8%) showed signs of fracture at 18 months, compared with 20% fracture rates at 24 months in the Sirocco trial.50

The Gore Viabahn stent graft and the eV3 (Covidien) Intracoil stent are also approved for SFA lesions, but the platform for both stents is slightly different than traditional scaffold nitinol stents. The Intracoil stent has an open coil design that allows for bending. Clinical data for the Intracoil demonstrated no improvement in nine-month revascularization rates versus balloon angioplasty (14.3% stent versus 16.1% balloon).52 As a result, the Intracoil has not experienced significant uptake.

The Viabahn stent is a covered stent composed of fabric and synthetic material supported by a metal mesh platform. Patency at one year using the Viabahn has been reported at 85% and 80% at two years, promising compared with Bard’s 83.2% at 12 months, as demonstrated in the Resilient trial. However, placemenent of a covered stent, such as the Viabahn, is noted to be difficult, and many interventionalists also note increased concerns with thrombosis with covered stents.53–54

The most anticipated news in SFA stenting is Cook Medical’s Zilver PTX paclitaxel-eluting nitinol self-expanding stent. The Zilver is currently the subject of an ongoing pivotal clinical trial studying its use in treating SFA lesions. The study is composed of 479 patients treated at 55 institutions. About half of the patients received the Zilver PTX paclitaxel-eluting stent, and the other half received angioplasty alone. Two-year results from the Zilver PTX trial were released in January 2011. Results show that the Zilver PTX demonstrated sustained patency of 83.1% at one year and 74.8% at two years.57 The angioplasty was not followed after the first year, when only 32.8% of patients demonstrated sustained patency.56

While the Zilver PTX trial again demonstrates the benefit of using stents over standalone balloon angioplasty in the SFA, it does not clearly demonstrate a benefit to using drug-eluting stents over bare-metal stents in the SFA. Further, although tempting, it is difficult to draw conclusions by comparing results of the Zilver PTX trial with results of Bard’s Resilient trial. Each trial treated patients with lesions of slightly different sizes, and each trial’s definition of patency is slightly different.

At least 19 additional companies are developing stenting technologies for use in treating SFA and tibial occlusions. However, several companies are also looking toward drug-eluting angioplasty balloons as a potential tool for treating PVD. While drug-eluting balloons are under consideration as a means of treating in-stent restenosis and small vessels in the coronary, they are still under consideration for treating primary lesions in the periphery. Studies being conducted in Europe are reviewing the use of balloons as a standalone device and as a means of pretreating an occluded vessel before delivery of a bare-metal stent. The question that remains is whether a drug can be successfully transferred from the surface of the balloon to the vessel wall in a way that allows the drug to remain in the vessel wall after the balloon is removed. At least 16 have drug-eluting balloon programs underway, with Medtronic and B. Braun leading the way.

|

|---|

Figure 5. Transapical and transfemoral approach is illustrated. |

Regardless of FDA’s decision on Cook’s Zilver PTX drug-eluting stent, it is clear that the market for endovascular products used in the periphery is growing rapidly and will continue to grow. eV3 estimates that there are a total of 900,000 endovascular procedures performed in the peripheral vasculature each year, the majority of which are stenting and angioplasty procedures.57 The company also estimates the worldwide market for stents used in the peripheral vasculature at $950 million and the worldwide market for angioplasty balloons used in the peripheral vasculature at $450 million.58 eV3 estimates market growth of approximately 7% per year.59 However, if clinical trials for more expensive drug-eluting devices begin to demonstrate clinical advantage, the market could expand by multiples of its current size.

Conclusion

Over the past 10 years, medtech innovation transformed the standard of care within many disease categories. Traditionally viewed as an option for only the most severe patients, devices have taken front stage, competing with and, in some cases, supplanting drug therapy as the optimal mode of treatment. The onset of minimally invasive endovascular technologies has decreased the stigma associated with having a medical procedure performed. Open surgical procedures that result in long recovery periods and significant discomfort are being replaced by minimally invasive procedures that allow patients to resume normal living within days.

Expect to see medical device innovation continue to grow in the coming years, as evidenced by the pool of development stage companies investing in device innovation for the treatment of heart disease and peripheral vascular disease. Despite potential setbacks resulting from the healthcare reform tax, major markets that are currently undeveloped or underdeveloped will increase the overall size the medtech industry. For example, percutaneous aortic and mitral heart valves are expected to open up heart valve procedures to patient groups that were not previously considered eligible for such procedures. Similar access to new patient groups is likely to result from advances in technologies used to treat PVD. In both cases, medical innovation is helping to develop new markets for new patient groups, as opposed to merely shifting procedure volume. This type of innovation is likely to drive overall market growth while improving outcomes for patients and physicians.

Entrepreneurs are likely to continue investing in device innovation for at least two reasons: Devices offer a more consistent and predictable pathway to market than drug therapies, and devices offer a more predictable return on invested capital than drug therapies. While devices are not typically associated with the blockbuster returns of the most successful drug therapies, clinical trials for Class III devices are typically smaller, shorter, and less expensive than those for new pharmaceutical agents. This is likely to drive investment for the medtech industry as capital markets and private investors continue to place value on the promise of near-term earnings that require a short investment window.

Acquisitions, licensing, and big-ticket litigation—all signs of a healthy and robust industry—have started to rebound and are likely to pick up considerably as large device companies look to invest their large cash reserves and protect their existing investments. Covidien’s recent acquisition of eV3 for $2.6 billion in cash is just one example of a large device company placing its bets.60 Medtronic’s acquisition of Invatec for $350 million plus milestone payments is another example of large device companies staking their claim in these high-growth markets.61

|

|---|

Figure 6. Peripheral vasculature in the leg is illustrated. |

Some likely plays in the coming years may involve J&J and Boston Scientific, both of which have noticeable gaps in the percutaneous valve space. Although neither company has traditionally focused on heart-valve technology, a transcatheter product solution for valve disease would fit well with their current offerings and sales capabilities. Similarly, some traditional competitors in the heart-valve space, such as St. Jude Medical, are conspicuously absent from the list of companies competing to release products within the next two to three years. St. Jude recently acquired AGA Medical to increase its footprint, but additional acquisitions may help accelerate its presence in the space.

It is clear that medtech investment and innovation will continue as medtech investors and entrepreneurs alike carry out their search for the next da Vinci robot. The spectacular developments that took place over the past decade have already demonstrated the returns that await first-movers and often those who are second, third, and even fourth to market. Recent clinical data has shown promising advances in key growth markets, and few will be content to sit on the sidelines as these technologies change the standard of care. The question that remains is not whether medtech innovation and investment will continue. The opportunities abound, extending far beyond the technologies discussed here. Capital will, without question, continue to flow into the hands of the right entrepreneurs, and the industry will continue to grow. The task at hand is identifying those entrepreneurs who are capable of grasping the opportunity.

Kevin O’Keeffe is an associate principal in the life sciences practice at Charles River Associates (Boston, MA).

References

1. Comparative Effectiveness Hits Medical Devices, [online] (Irvine, CA: Medtech Insight, 2010) [cited 17 June 2010]; available from Internet: www.medicaldevicestoday.com/2010/06/comparative-effectiveness-hits-medical-devices.html.

2. U.S. Medical Device Market Estimated at $94.9 Billion in 2010, [online] (Princeton, NJ: Espicom) [cited 18 April 2010]; available from Internet: www.espicom.com/Prodcat2.nsf/Product_ID_Lookup/00000110?OpenDocument.

3. Cardiovascular Market Growth Trends, [online] (Huntingdon Valley, PA: The Free Library, 2010 [cited 1 September 2010]); available from Internet: www.thefreelibrary.com/Cardiovascular+market+growth+trends.-a0238750564.

4. “Orthobiologics is the fastest growing segment of the $33 billion global orthopedic market,” [online] companiesandmarkets.com [cited 10 September 2010]; available from Internet: www.companiesandmarkets.com/news/orthobiologics-is-the-fastest-growing-segment-of-the-33-billion-global-orthopedic-market-n126.aspx.

5. “The changing face of Abbot,” [online] [cited 4 June 2010]; available from Internet: www.fool.com/investing/general/2010/06/04/the-changing-face-of-abbott.aspx.

6. Bloomberg closing prices for Bloomberg tickers: S5HCEP, SPX, S5PHAR.

7. PhRMA, “New Drug Approvals in 2009,” [online] [cited 28 March 2011]; available from Internet: www.phrma.org/sites/default/files/422/nda2009.pdf. Note, this is a 2010 article citing 2007 Study by the Tufts Center for the Study of Drug Development.

8. “Medical Technology Development Costs Cause Concern In US,” [online] [cited 14 October 2010]; available from Internet: medical-technologyblog.com/medical-technology-development-costs-cause-concern-in-us.

9. AV Kaplan, MD, et al. “Medical Device Development, From Prototype to Regulatory Approval,” Circulation, 2004, [cited 28 March 2011]; available from Internet: http://circ.ahajournals.org/cgi/content/full/circulationaha;109/25/3068.

10. The Medical Technology Blog. News and Views on the Medical Technology Industry. [cited 28 March 2011]; available from Internet: http://medical-technologyblog.com/medical-technology-development-costs-cause-concern-in-us.

11. Stephen Berberich, “Biotechs outsource to cut costs” in Gazette.net, [online] 28 August 2009 [cited March 14, 2011]; available from Internet: www.gazette.net/stories/08282009/businew175554_32526.shtml. and Life Sciences World, “Phase 3 Clinical Trial Costs Exceed $26,000 per Patient,” cited 14 March 2011; available from Internet: www.lifesciencesworld.com/news/view/11080.

12. “Comparative Effectiveness Hits Medical Devices,” Medtech Insight, 17 June 2010.

13. FDA and Nature Reviews, Drug Discovery.

14. “Medical Devices: FDA Should Take Steps to Ensure that High-Risk Device Types Are Approved through the most Stringent Premarket Review Process,” [online] US Government Accountability Office, cited 28 March 2011; available from Internet: www.gao.gov/products/GAO-09-190.

15. J.P. Morgan, “Cardiovascular Devices, TCT 2009 Preview,” 10 September 2009.

16. Shawn Tully, “The (second) worst deal ever,” in CNN Money [online] 5 October 2006 [cited 28 March 2011] available from Internet: http://money.cnn.com/magazines/fortune/fortune_archive/2006/10/16/8390284/index.htm.

17. “Medtech Analyzer,” Credit Suisse, January 2010.

18. Barry Meier, “Boston Scientific to Pay $1.7 Billion to Settle Patent Suits,” in New York Times [online] 1 February 2010 [cited 14 March 2011]; available from Internet: www.nytimes.com/2010/02/02/business/02device.html.

19. “Late Stent Thrombosis,” Angioplasty.org, [online] [cited 14 March 2011]; available from Internet: www.ptca.org/articles/patients_late_stent_thrombosis.html.

20. Intuitive Surgical 2009 Form 10-K.

21. “Investor Presentation Q2 2010,” Intuitive Surgical, [online] [cited 16 March 2011]; available from Internet: http://phx.corporate-ir.net/External.File?item=UGFyZW50SUQ9NTUyMDB8Q2hpbGRJRD0tMXxUeXBlPTM=&t=1.

22. Intuitive Surgical Fourth Quarter 2010 Earnings Transcript.

23. Intuitive Surgical 2009 Form 10-K.

24. J.P. Morgan, “Cardiovascular Devices,” 10 September 2009, TCT 2009 Preview.

25. “U.S. Food and Drug Administration Clears Way for Multi-Center Clinical Trial of Hansen Medical Sensei X Robotic Catheter System for Treatment of Atrial Fibrillation,” Hansen Medical, press release, 1 November 2010.

26. “U.S. Market for Cardiovascular Devices,” iData Research Inc., August 2009.

27. Percutaneous Aortic Valve Replacement, [online] (Boston: Brigham and Women’s Hospital, [cited 28 March 2011]); available from Internet: www.brighamandwomens.org/Departments_and_Services/surgery/services/cardiacsurgery/pavr.aspx.

28. Mary Thompson, “Heart Valve Market: PAVR Posed for Growth,” Medtech Insight, January 2009.

29. Edwards Lifesciences, Second Quarter, 2010; Form 10-Q.

30. Orange County Business Journal, [online] cited 28 March 2011, available from Internet: www.ocbj.com/news/2010/oct/03/valves-sales-europe-spur-edwards-optimisms.

31. “Edwards SAPIEN XT Transcatheter Valve and Delivery Systems Receive CE Mark,” Edwards Lifesciences, [cited March 2010]; available from Internet: www.edwards.com/eu/newsroom/ShowPR.aspx?PageGuid=%7Bcd591bb8-93da-444a-9e8d-54f0f4f3e388%7D.

32. Omar Ford, “Medtronic gets FDA nod for CoreValve IDE clinical study,” in Medical Device Daily [online] [cited 16 March 2010]; available from Internet: www.medicaldevicedaily.com/servlet/com.accumedia.web.Dispatcher?next=bioWorldHeadlines_article&forceid=73202.

33. “CoreVale Receives CE Mark Approval for its ReValving System and Announces Plans to Initiate,” AllBusiness [online] 16 May 2007 [cited 16 March 2011]; available from Internet: www.allbusiness.com/services/business-services/4332758-1.html.

34. “Medtronic Gains CE Mark for Enhanced Corevalve Delivery Catheter System with Accutrak Stability Layer,” [online] [cited 16 March 2011]; available from Internet: www.medicalnewstoday.com/articles/200199.php.

35. “Sorin Group receives CE mark Approval for the Innovative Self-Anchoring Aortic Heart Valve, Perceval S.,” Sorin Group [online] 31 January 2011 [cited 9 June 2011]; available from Internet: www.sorin.com/press-release/sorin-group-receives-ce-mark-approval-innovative-self-anchoring-aortic-heart-valve-perceval-s.

36. “The New England Journal of Medicine Publishes Transcatheter Heart Valve Trial Results,” Edwards Lifesciences press release, [online] [cited 28 March 2011]; available from Internet: www.edwards.com/es/newsroom/Pages/ShowPR.aspx?PageGuid={1981375d-3f20-4ada-9bb3-69aa519b1d81}.

37. Edwards Lifesciences investor presentation; 10 December 2009.

38. Edwards Lifesciences investor presentation; 13 December 2010.

39. M Thompson, “Percutaneous Heart Valve Technology, The Mitral Challenge,” Medtech Insight, [online] February 2009.

40. MitraClip Mitral Valve Repair System, [online] (Abbott Park, IL: Abbott Vascular [cited 28 March 2011]); available from Internet: www.abbottvascular.com/int/mitraclip.html#learn-more.

41. “New Data Demonstrates Abbott’s Investigational MitraClip System Has Potential to be a Valuable Treatment Option for Patients with Mitral Regurgitation, the Most Common Heart Valve Condition,” [online] 14 March 2010 [cited 9 June 2011]; available from Internet: www.abbott.com/global/url/pressRelease/en_US/60.5:5/Press_Release_0830.htm.

42. “Heart-Valve Win May Prod J&J, Abbott to Buy Companies,” in Bloomberg [online] 10 November 2010 [cited 9 June 2010]; available from Internet: www.bloomberg.com/news/2010-11-10/heart-valve-win-may-prod-j-j-abbott-to-shop-for-technology.html.

43. DL Dawson, MD and WR Hiatt, MD, “Peripheral Arterial Disease: Medical Care/Complications: Prevalence of PAD,” in Medscape [online] [cited 28 March 2011]; available from Internet: www.medscape.com/viewarticle/438770_2.

44. eV3 investor presentation, 23 March 2010, [online] cited 28 March 2011; available from Internet: http://phx.corporate-ir.net/External.File?item=UGFyZW50SUQ9MzczODYwfENoaWxkSUQ9MzcxNzcxfFR5cGU9MQ==&t=1.

45. Peripheral Vascular Disease: The Silent Killer, [online] (Columbus, OH: Ohio Health, Riverside Methodist Hospital, [cited 28 March 2011]); available from Internet: www.ohiohealth.com/bodyriverside.cfm?id=4002.

46. AJ Feiring, MD, “Antegrade popliteal artery approach for the treatment of critical limb ischemia in patients with occluded superficial femoral arteries” in Hemodinamiadelsur [online] 29 October 2007 [cited 28 March 2011]; available from Internet: www.hemodinamiadelsur.com.ar/journals/journal_118.asp.

47. Peripheral Arterial Disease—Statistics, [online] (Dallas, TX: American Heart Association), [cited 28 March 2011]; available from Internet: www.americanheart.org/downloadable/heart/1136822690283PAD06%20REVdoc.pdf.

48. M Kass, MD and CA Glover, MD, “Lesion Characteristics and Coronary Stent Selection with Computed Tomographic Coronary Angiography: A Pilot Investigation Comparing CTA, QCA and IVUS,” in The Journal of Invasive Cardiology [online] July 2010 [cited 28 March 2011]; available from Internet: www.invasivecardiology.com/articles/Lesion-Characteristics-and-Coronary-Stent-Selection-with-Computed-Tomographic-Coronary-Angi (see Figure 1).

49. SIROCCO Trial Shows Minimal Long-Term Restenosis Rates With Cordis S.M.A.R.T. Stent [online] 23 February 2011 [cited 28 March 2011]; available from Internet: www.prnewswire.co.uk/cgi/news/release?id=191508.

50. Bard Lifestent label, [cited 28 March 2011]; available from Internet: www.accessdata.fda.gov/cdrh_docs/pdf7/P070014c.pdf.

51. Bard Receives FDA Approval for the Lifestent Vascular Stent [online] 17 February 2009 [cited 28 March 2011]; available from Internet: www.bardpv.com/press-lifestent.php.

52. GM Ansel, MD, “Using Coiled Stents to Treat Arterial Occlusive Disease, June 2003,” Endovascular Today [online] June 2003 [cited 28 March 2011]; available from Internet: http://bmctoday.net/evtoday/2003/06/article.asp?f=0503_091.html.

53. S Banerjee, MD and ES Brilikas, MD, PhD, “Covered Stents for the Treatment of SFA Occlusive Disease,” Endovascular Today, [online] October 2008 [cited 28 March 2011]; available from Internet: http://bmctoday.net/evtoday/2008/10/article.asp?f=EVT1008_04.php and CJ White, MD.

54. WA Gray, MD, Circulation, “Endovascular Therapies for Peripheral Arterial Disease, An Evidence Based Review, 2007,” Advances in Interventional Cardiology [online] 6 November 2007 [cited 28 March 2011]; available from Internet: http://circ.ahajournals.org/cgi/content/full/116/19/2203.

55. “Cook Medical’s 2-Year Zilver PTX Trial Results Presented at ISET, January 2011,” Endovascular Today [online] 17 January 2011 [cited 28 March 2011]; available from Internet: http://bmctoday.net/evtoday/2010/11/article.asp?f=two-year-zilver-ptx-trial-results-presented-at-iset.

56. ISET, “Two-Year Zilver PTX Trial Results Show Drug-Coated Stents Keep Leg Arteries Open,” (paper presented at ISET 2011, 16–20 February, Miami Beach, 2011).

57. eV3. (2009) Form 10-K for the fiscal year ended December 31, 2008.

58. eV3 investor presentation from May 11, 2010, [online] (Plymouth, MN: ev3 Endovascular, 2010 [cited 28 March 2011]); available from Internet: http://phx.corporate-ir.net/External.File?item=UGFyZW50SUQ9MzgyODkwfENoaWxkSUQ9MzgzODkxfFR5cGU9MQ==&t=1.

59. eV3 investor presentation from May 27, 2010, [online] (Plymouth, MN: ev3 Endovascular, 2010 [cited 28 March 2011]); available from Internet: http://phx.corporate-ir.net/External.File?item=UGFyZW50SUQ9Mzg0Mzc0fENoaWxkSUQ9Mzg1ODM2fFR5cGU9MQ==&t=1.

60. Jennifer Rossa, “For Warburg, Covidien’s Ev3 Deal Offers Long Awaited Exit,” Wall Street Journal [online] 28 March 2011 [cited 28 March]; available from Internet: http://blogs.wsj.com/privateequity/2010/06/01/for-warburg-covidiens-ev3-deal-offers-long-awaited-exit.

61. Medtronic to Acquire Invatec and Affiliated Companies, [online] (Fridley, MN: Medtronic, 25 January 2010 [cited March 28, 2011]); available from Internet: wwwp.medtronic.com/Newsroom/NewsReleaseDetails.do?itemId=1264427238226&lang=en_US.

About the Author(s)

You May Also Like