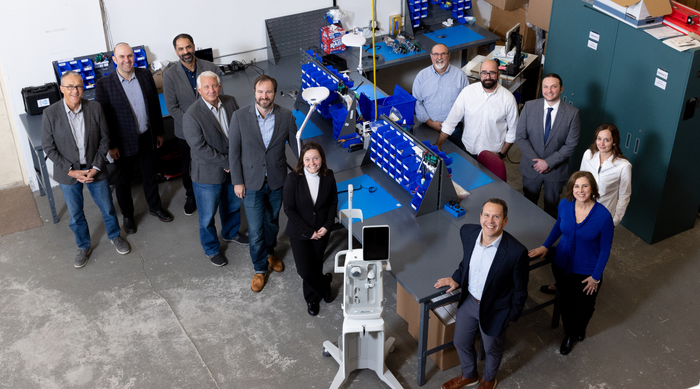

Photo of Reprieve Medical team with the company's diuretic and fluid management system for acute decompensated heart failure.

StartupsNew Cardiovascular Company Emerges from Stealth ModeNew Cardiovascular Company Emerges from Stealth Mode

Fresh off a $42 million series A financing, Reprieve Medical is developing an intelligent automated fluid management system for heart failure patients.

.png?width=300&auto=webp&quality=80&disable=upscale "NeuroStar")

.png?width=300&auto=webp&quality=80&disable=upscale "Two Winners Chosen for APCI, MedTech Color ‘Make Your Medical Device Pitch for Kids!’ Competition")

.png?width=300&auto=webp&quality=80&disable=upscale "Siemens Healthineers")

.png?width=300&auto=webp&quality=80&disable=upscale "M&A")

.png?width=300&auto=webp&quality=80&disable=upscale "Medtronic's Aurura EV ICD (extravascular implantable cardioverter-defibrillator) is designed with the lead placed outside of the heart and veins")

.png?width=300&auto=webp&quality=80&disable=upscale "Michael Monovoukas")

.png?width=300&auto=webp&quality=80&disable=upscale "Female medical professional treating patient")

.png?width=300&auto=webp&quality=80&disable=upscale "M&A")

.png?width=300&auto=webp&quality=80&disable=upscale "Baxter International")

.png?width=300&auto=webp&quality=80&disable=upscale "Layoffs")

Editors' Choice

Sign up for the QMED & MD+DI Daily newsletter.